Vesting periods are anti-worker

They don't shape employee behavior (including teachers)

Early in my career, I made a big financial mistake.

At my first professional job I was offered a retirement plan with a 3-year vesting period. If I stayed at least three years, I would “vest” and qualify for my employer’s 4% contributions into my retirement account. If I left before the 3-year mark, I would forfeit all or most of those contributions.

I don’t remember the exact specifics anymore, but I was offered a new job somewhere around month 32 or 33. I was only a few months short of vesting, but the new job came with a significant pay raise, and it was a great opportunity. I couldn’t pass it up, and I don’t regret taking it. But it cost me several thousand dollars in foregone retirement savings.

In theory, a vesting period can act as a retention incentive. In my case it wasn’t enough, but do vesting periods generally shape employee behavior?

The answer, according to a recent analysis from Vanguard, is no. They looked at a sample of 1,399 plans offering a range of different vesting schedules, and they analyzed the departure decisions of 3,758,582 workers. (That’s not a typo, the sample really was that big.) The image below summarizes their results.

On the left side are the months leading up to a vesting requirement. If it had an impact, we should see lower turnover rates leading up to vesting—that is, people should stick around in order to qualify for employer retirement contributions.

And on the right side of the graph, we should see higher turnover. If there were people sticking around solely to qualify for retirement benefits, we should see higher turnover after they passed the vesting point. But the Vanguard data don’t show either of these things. In fact, they find a null result: vesting schedules do not appear to have any effect on participants’ separation decisions.

In the longer paper, the authors find no differences across age or income of the workers or the length of the vesting period. They also find no difference for workers with larger balances in the plans. They write, “We expect the effects of vesting incentives, if they exist, to be larger for participants with larger employer contribution balances. But again, we find that the null effect holds across the distributions of absolute and relative employer balances.”

In fact, they find a null effect even for participants who stand to lose employer contributions worth more than 10% of their annual income.

In other words, I wasn’t so different from everybody else. Employees don’t take vesting periods into account when considering career moves. That makes me feel a little bit better about my own decision back in my 20s…

Vesting periods and teachers

But what about teachers? Do vesting periods shape teacher behavior?

If so, we should see it in pension plan withdrawal rates. Pension plans use their historical data to make future projections, and those projections feed into the plan’s estimates for how much money they will need to pay future benefits.

Say a state has a 5-year vesting period. If teachers truly valued their pension benefit, there should be some contingent of 4-year veterans who stick it out one more year just to reach that fifth year. But when I looked at this question with Kelly Robson Foster, we could not find a single state that operationalizes this in their withdrawal assumptions.

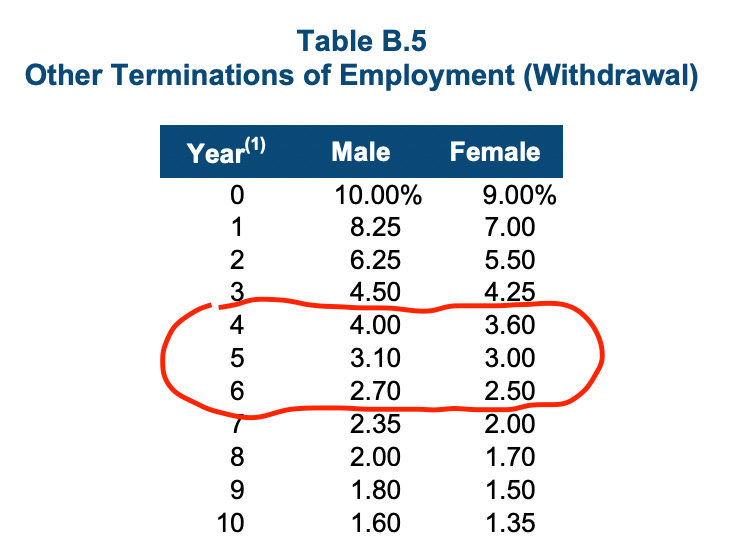

I’ll show you a couple. First up is California. They have a five-year vesting requirement. And yet here are their withdrawal rate assumptions. As you can see, they assume a bigger drop-off from four to five years than they do from years five to six. This is exactly opposite of what you’d expect if California teachers were somehow sticking around to qualify for a CalSTRS pension. Instead, it looks more like a fairly steady decrease, and the pension incentive is doing nothing at all.

Or here’s Illinois. They have a 10-year vesting period for all workers hired in 2011 or later, and yet they don’t even bother looking at withdrawal rates around the 10-year mark. Instead, they break up their withdrawal assumptions into two big categories, those with less five years or service and those with five or more years of service. Again, they’re making consequential financial decisions and completely ignoring their vesting requirement.

So what?

If vesting periods don’t affect retention, then what purpose are they serving?

The answer to that is pretty obvious. Remember my story, about how I forfeited a few thousand dollars when I failed to fully vest at my first professional job? Well, my employer got to keep that money. That is, vesting periods should be seen as little more than a way for employers to save money. And this is where public school teachers are really getting screwed.

In private sector, half of all 401k plans allow for immediate vesting, and federal law requires that employees receive at least some share of their employer’s contribution after no more than three years.

There is no such law protecting public school teachers, and they face much steeper vesting requirements. When Andy Rotherham and I looked at this a few years ago , we found only one state (Arizona) offered immediate vesting, 24 states and the District of Columbia required teachers to stay for five years, and another 17 required them to stay ten years. And, when we used the state withdrawal assumptions to see how many starting teachers actually met their state’s vesting requirement, we found that it was about half. Half of all starting teachers vest into their state-funded pension plan, and half do not.

Teacher advocates and teachers unions should be upset about this. And they should be doubly upset in the states with 10-year vesting requirements. Those 10-year requirements would be illegal in the private sector, and yet supposedly teacher-friendly states like Illinois, Massachusetts, and Connecticut require teachers to serve for 10 years before qualifying for retirement benefits.

Worst of all, these states also don’t provide Social Security coverage. A teacher could work for nine years and have no pension and no Social Security. That’s shameful. If state legislators wanted to actually move beyond #HashtagsForTeachers, they should drop their vesting requirements.

Who decides the terms of the pension plans? Do the unions participate in negotiation of the terms? A longer vesting period is, in isolation, obviously worse for teachers. However, I can imagine longer tenured teachers (who compose the majority of union votes) preferring to trade a longer vesting period for higher payouts in retirement or other concessions. Unions have a tendency to entrench guild-like tenure based compensation and this could be an example.