Oklahoma's Painful Pension Promises

The finances are better. The benefits aren’t.

I have a new piece out at The 74 this week looking at a painful choice facing Oklahoma legislators. For folks outside of the Sooner state, one thing to know is that Oklahoma has been a standout on the teacher pension funding front:

Thanks to a combination of benefit cuts, plus a surge of new contributions, it has dramatically improved the health of its teacher pension plan.

For example, the system’s unfunded liability, essentially the difference between how much it had promised and how much it had saved toward those promises, shrank from $10.4 billion in 2010 down to $6.1 billion last year. Its funded ratio — a comparison between its assets and its liabilities — has improved from 47% in 2010 all the way up to 80% as of last June.

A big part of that progress has come from a huge surplus of contributions, thanks to special levies on the state’s sales taxes, cigarette taxes, corporate income taxes, individual income taxes and lottery proceeds. This extra state contribution came out to $456 million last year, and now state legislators are wondering if they can cut back just a bit.

Read my full piece for more on how they would use that money.

But are all those pension costs good for workers?

Here I want to talk about one other aspect, which is what all this money is paying for. Namely, Oklahoma’s teacher pension plan is quite costly, but it also kind of sucks? In fact, Oklahoma offers far worse retirement plans to K-12 teachers than it offers to other types of public servants.

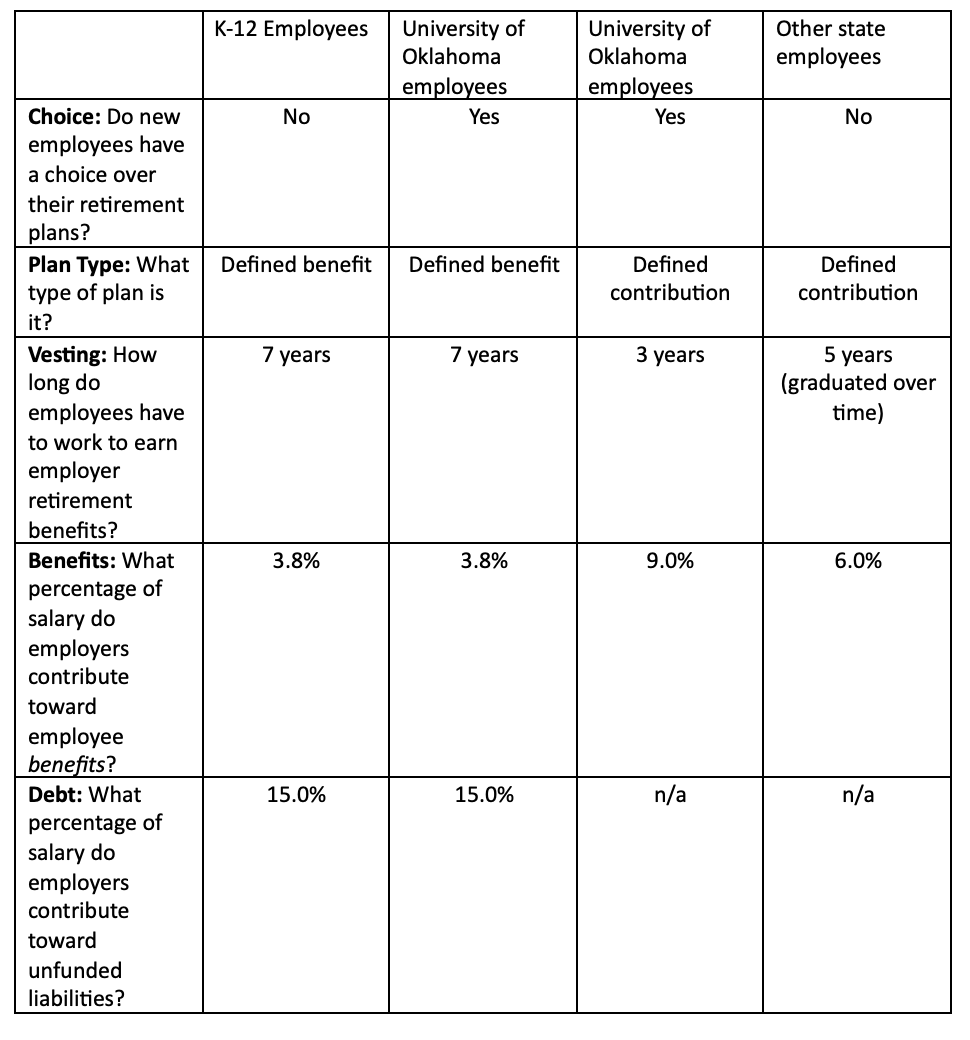

This might surprise some people. But I created a simple table below to help compare the retirement benefits that Oklahoma offers its K-12 teachers versus the retirement plan it offers University of Oklahoma employees and other state workers.

First is the matter of choice. Do employees get a choice over what type of retirement plan they get? In K-12, the answer is typically no. In higher ed, the answer is often yes. And at the University of Oklahoma, new employees get a choice between the same defined benefit retirement plan that K-12 teachers have, or they can choose a defined contribution plan (a 401k).

How long do workers have to stay before qualifying for at least some share of their employer’s contributions? This is called the “vesting” period, and it’s set at seven years for K-12 teachers. That is, a teacher who leaves after five years gets no employer-provided retirement benefits. Both defined contribution plans are shorter, and a new bill would drop it entirely for state employees.

But what about costs and benefits? These are a bit tricker to compare across plan types, so I’ve broken out the costs of the defined benefit plans into two different components. The first is called the plan’s “normal cost” of benefits, or the plan’s own estimates about how much it needs to contribute today in order to pay the promised benefits in the future. Essentially, this is the plan’s estimate for how much its benefits are worth, on average across all of its members.

This is where it becomes obvious that K-12 teachers are getting a raw deal. On average across all K-12 teachers, the value of their employer-provided benefits comes out to just 3.8% of salary—roughly what a basic private-sector 401(k) might offer.

In contrast, the public-sector defined contribution plans are much more generous. State employees get a 6% match, while University of Oklahoma employees get 9%.

But defined benefit pension plans also carry a second cost when they’re not fully funded. These unfunded liabilities are essentially a form of debt, and they reflect the plan’s estimate for how much it should be contributing today in order to reach full funding in the future.

Note that defined contribution plans do not have this type of debt. They make no promises about the future, so the full employer contribution goes toward employee benefits.

Across all of these categories, Oklahoma’s higher education employees have the best retirement plan options. Not only can they pick a plan that’s right for them, they at least have access to a low-cost, high-quality defined contribution plan. If I were choosing, I’d want that one.

Reading List

Lauren Wagner: This Texas Elementary Is Achieving High Reading Scores a Million Words at a Time

Ashley Zanchelli: When did school book fairs stop selling books?

Doug Lemov: We remember stories and are likely to think more deeply about information when we encounter it in a story.

Joshua Dwyer: The broken feedback loop keeping parents, students, and colleges in the dark

Harry A. Patrinos: “the highest returns [to education] come from bringing new learners into the system, including low-income students, rural populations, and first-generation learners.”

Will Austin: “For the first time in two decades, the reported average Massachusetts teacher salary has dropped below per capita income in Massachusetts.”

Tim Harford: Many people are sending texts that should have been emails