Education Jobs Update, April 2025

Public K-12 employment continues to hit new highs

Oof, have you checked your 401k lately? Better yet, don’t. But with the stock market melting down over the Trump tariffs, I wanted to take a closer look at the education labor market. Do we see any signs of problems yet?

The short answer is no. Job openings and hirings remain strong, layoffs are low, and turnover rates are coming down from their pandemic-era highs.

The stock market is not the jobs market, and the education market is once or twice removed from the private sector. Think of like a bullwhip. If the stock market tanks and we head into a recession, the first employees to feel the pain will be those exposed to super-cyclical sectors like retail, entertainment, or other luxury goods. But when fewer people are working and making money that means lower tax receipts, which then translates into less money for schools. But that process takes a while to play out, it’s a long tail, and it means that education budgets often trail the broader economy.

Within the education context, we’ve long been on the lookout for a potential “fiscal cliff” when the federal ESSER money runs out. Secretary McMahon put an abrupt halt to the late extensions of those funds, which could accelerate those trends somewhat.

However, there’s nothing showing up in the national numbers yet. In the jobs numbers released on Friday by the Bureau of Labor Statistics, public K-12 employment hit new all-time highs in both seasonal and non-seasonally-adjusted terms. While schools are serving fewer students than they did five years ago, they have more employees.

As you might expect, the education labor market is highly seasonal, so my favorite way to look at is without the seasonal adjustments. The chart below breaks it out by year. The dark black line is 2020. Things were chugging along normally until COVID hit in March, leading to an immediate drop in employment. The summer trough is always large in education, but when schools reopened virtually in the fall of 2020, they needed fewer part-time bus drivers and school custodians and lunchroom workers.

But then the first of the $190 billion in federal relief funds started rolling in, schools slowly got back to in-person services, and we’ve been in a slow climb ever since. 2021 was a bit higher than 2020, and so on. Here we are in 2025 (the red line), and schools continue to add employees at a slow but steady clip.

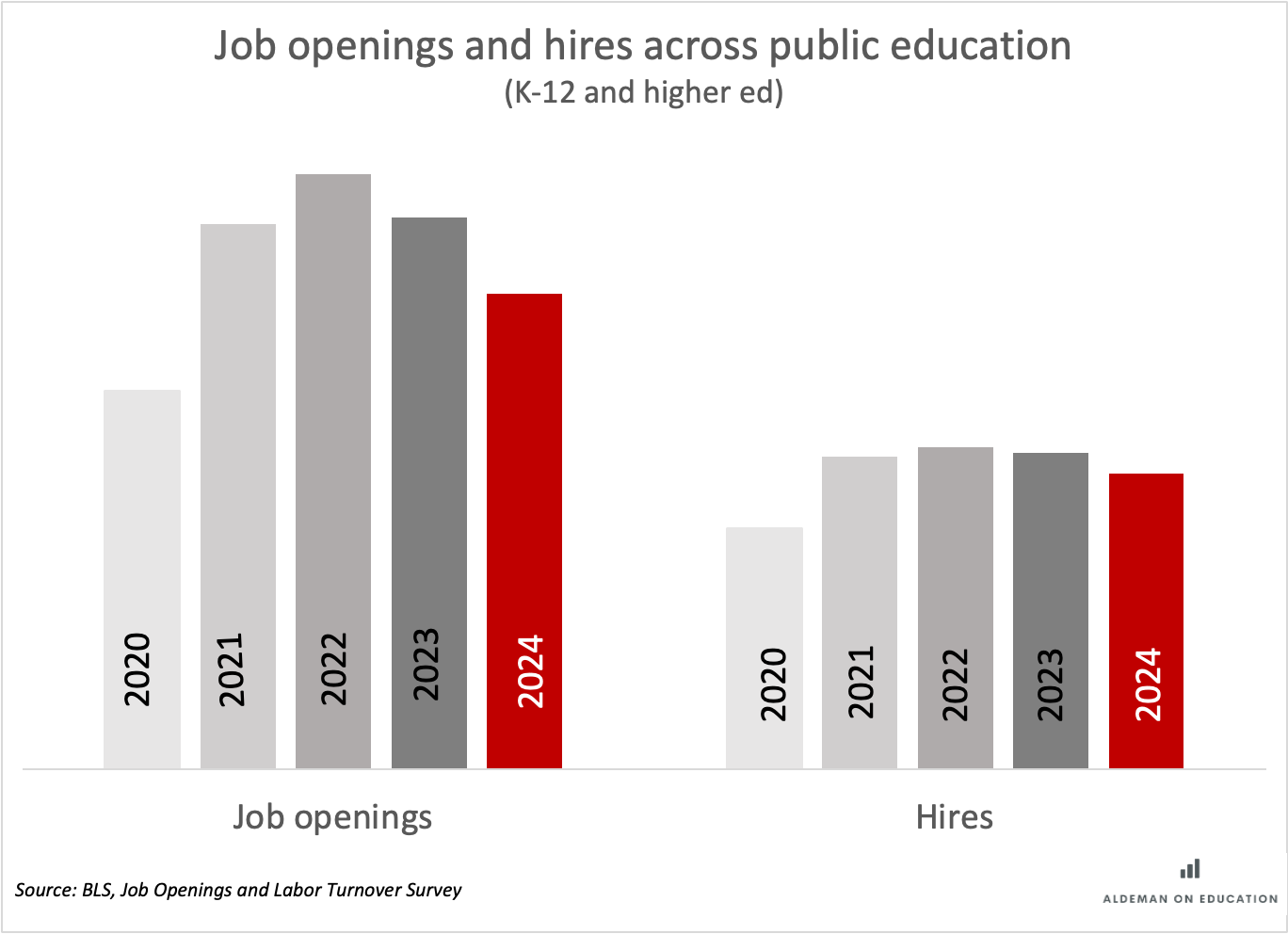

The BLS Job Openings and Labor Turnover (JOLTS) survey shows similar trends. Like employers in many other industries, schools had a huge surge of job openings in 20221 and especially 2022 and were unable to fill all of their vacancies. But those have slowly come back down, as have the hiring numbers.

We only have two months of JOLTS data for 2025 so far, and job openings are tracking just a bit higher than 2020 (pre-pandemic). It’s still early, but layoffs also don’t seem to be any higher than normal. Similarly, employee turnover rates in education peaked in the fall of 2022 and have been falling since then.

The last piece of data I want to throw at you is an update on what types of jobs were lost during the depths of the pandemic. The public K-12 industry is a pretty big one, with almost 8.5 million employees spread across a number of roles. The BLS data come out monthly, but they can’t tell us any more detail than those high-level industry totals. That is, they’re counting all jobs equally, and they lump together one full-time teacher alongside a part-time crossing guard or one afterschool assistant.

To get a deeper understanding of what has happened within education, I turned to the Census Bureau’s Annual Survey of Public Employment and Payroll (ASPEP). This is an administrative collection of all state and local payroll numbers, separated out by industry and broken out for full- versus part-time workers. Within education, it also breaks out “instructional” versus “non-instructional” roles. The survey is collected annually every March, and the chart below shows the change in roles since March 2019.

As you can see, the count of full-time staff, in both instructional and non-instructional roles in K-12 public education, dipped very slightly from 2020 to 2021, but those quickly recovered and continue to grow. Meanwhile, the number of part-time staff, in both instructional and non-instructional roles, fell dramatically and has not fully recovered. Meanwhile, the black line represents the number of Full-Time Equivalent workers (FTEs). It went negative from 2020 to 2021 but quickly recovered.

In numeric terms, schools lost about 82,000 full-time workers in that first year (a decline of 1.3%) while they lost 354,000 part-time staff (a decline of 21%). Since then, they’ve gained 284,000 full-time staff (a 4.6% gain) and added 241,000 part-time staff (a gain of 14.5%).

The lesson here is that part-time staffing roles are much more volatile, and schools are likely to make reductions there first before laying off full-time staff. We’re not there yet, but this might be useful to remember if and when the next recession hits..